When you trade, sell, or even give away cryptocurrency in the UK, the government isn’t just watching-it’s counting. Since October 2024, the rules have changed dramatically. If you’re holding crypto, you need to know exactly how much tax you owe. It’s not about whether you made money-it’s about whether you moved it. And that’s where most people get caught off guard.

What Counts as a Taxable Event?

HMRC doesn’t treat crypto like cash. It treats it like stocks or property. That means every time you dispose of it, you might owe tax. A disposal isn’t just selling for pounds. It includes:

- Exchanging one crypto for another (like ETH for BTC)

- Using crypto to buy goods or services

- Selling crypto for fiat currency (GBP, USD, etc.)

- Gifting crypto to anyone who isn’t your spouse or civil partner

Even swapping 0.1 BTC for 500 SOL counts. That’s a taxable disposal. Many people assume only cashing out triggers tax-but that’s not true. The UK system is built to catch every movement of value.

Capital Gains Tax: The £3,000 Limit

For the 2024/2025 and 2025/2026 tax years, your tax-free allowance for capital gains is £3,000. That’s down from £6,000 last year, and £12,300 in 2020. This drop means far more people are now paying tax.

If your total crypto gains across all disposals in a year exceed £3,000, you pay Capital Gains Tax (CGT) on the amount over that threshold. The rate depends on your income:

- 18% if you’re a basic-rate taxpayer (income up to £50,270)

- 24% if you’re a higher or additional-rate taxpayer (income over £50,270)

These rates apply only to disposals made on or after October 30, 2024. Before that, rates were 10% and 20%. So if you sold crypto in November 2024, you paid 8% more than you would have a year earlier.

Here’s a real example: You bought 1 ETH for £2,000 in January 2023. In March 2025, you sold it for £3,500. That’s a £1,500 gain. You also traded 0.5 BTC (bought for £10,000) for 100 SOL (worth £12,000) in June 2025. That’s another £2,000 gain. Total gains: £3,500. You’ve gone over the £3,000 allowance by £500. You owe CGT on that £500. At 18%, that’s £90. If you’re a higher-rate taxpayer, it’s £120.

Income Tax: When Crypto Is Pay

Not all crypto activity is treated as capital gain. If you earn crypto as income, it’s taxed as regular income. That includes:

- Staking rewards

- Mining rewards

- Airdrops you didn’t request but received

- Crypto paid as salary or freelance income

This income is added to your total earnings for the year. You pay Income Tax at your normal rate: 20%, 40%, or 45%, depending on your total income. The personal allowance is £12,570 for 2024/2025-meaning you don’t pay tax on the first £12,570 of income. But crypto earnings count toward that total.

Example: You earn £40,000 in salary and £3,000 in staking rewards. Your total income is £43,000. The £3,000 in staking is taxed at 20% because it pushes part of your income into the higher bracket. You owe £600 in income tax on those rewards alone.

How to Track Your Transactions

HMRC requires you to keep detailed records for every crypto transaction. You need:

- Date of acquisition

- Cost basis (what you paid, including fees)

- Date of disposal

- Proceeds from disposal (what you received)

- Transaction fees paid

That’s not just for sales. It’s for every swap, every airdrop, every purchase with crypto. If you used Coinbase, Binance, and Kraken, you’ve got data scattered across three platforms. Manually tracking 500+ transactions? That’s what 87% of UK crypto investors reported doing in early 2025. One Reddit user spent 40 hours on their 2024/2025 return.

Most people use crypto tax software now. Tools like Koinly, CoinTracker, and Blockpit auto-import from exchanges and calculate your gains. In 2025, 62% of UK crypto holders used these tools-up from 38% in 2023.

The ‘Same-Day Rule’ and ‘Bed and Breakfasting’

HMRC has strict matching rules to stop people from gaming the system. If you buy and sell the same crypto on the same day, those trades are matched first. If you sell crypto and buy it back within 30 days, the system forces you to match the disposal with the new purchase. This is called ‘bed and breakfasting,’ and it’s blocked.

Why does this matter? Let’s say you sell 1 BTC for £50,000 on Monday. You buy it back on Wednesday for £48,000. HMRC doesn’t let you claim a £2,000 loss. They treat it as one transaction. Your cost basis resets to £48,000. This makes timing trades harder-and more expensive if you’re trying to harvest losses.

What You Can’t Do

You can’t use capital losses to reduce your income tax. If you lost £5,000 on crypto trades this year, you can’t subtract that from your salary. But you can carry those losses forward forever to offset future capital gains. So if you make £10,000 in gains next year, you can use £5,000 of last year’s loss to reduce your tax bill.

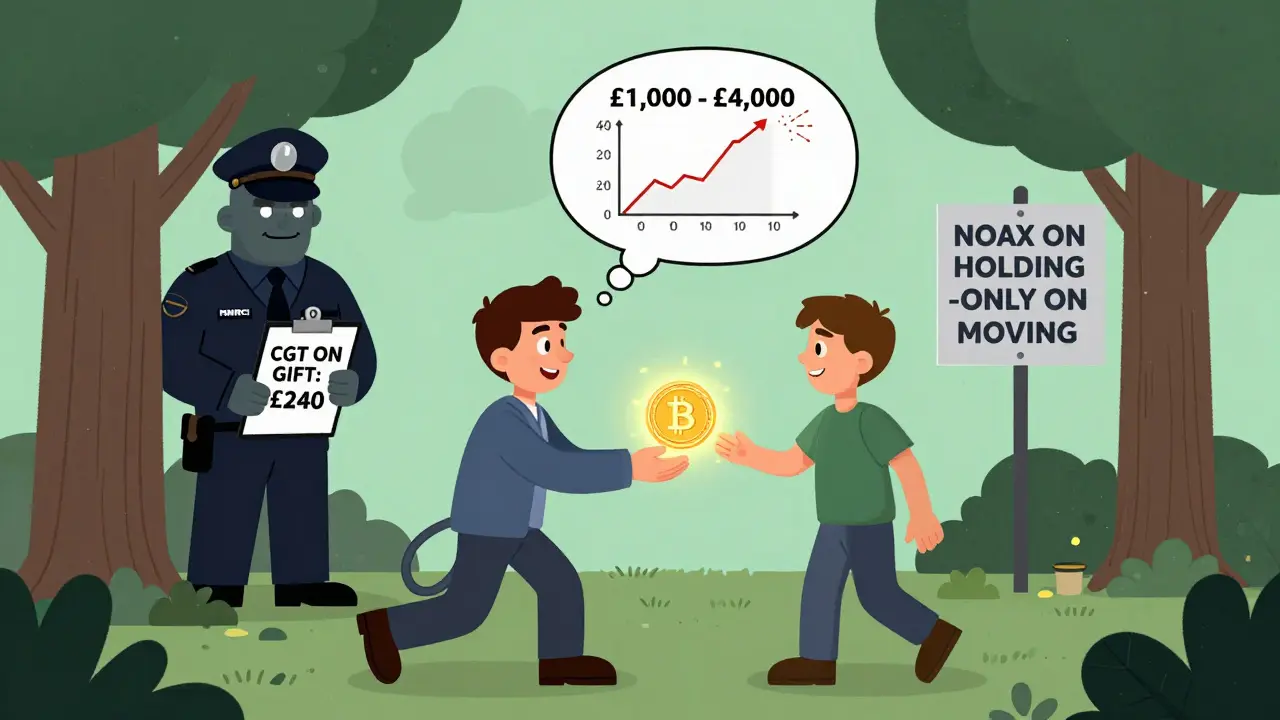

Also, gifting crypto to family members (other than your spouse) triggers a disposal. That means you owe CGT on the gain at the time of the gift. One user on Reddit thought gifting £4,000 in ETH to his brother was tax-free. He didn’t realize the ETH had risen from £1,000 to £4,000. He owed £240 in CGT.

Reporting Deadlines and Penalties

You must report crypto gains on your Self-Assessment tax return. The deadline is January 31st after the end of the tax year (which runs April 6 to April 5). If you miss it, you face automatic penalties and interest.

HMRC is getting smarter. Since 2022, they’ve been collecting data from crypto exchanges. In January 2025, 47 UK-based exchanges were required to report user transaction data. By January 2026, all exchanges operating in the UK must comply. That means HMRC will soon have a full picture of your trades-whether you report them or not.

What’s Coming Next?

The Financial Conduct Authority (FCA) approved crypto exchange-traded notes (ETNs) in October 2025. That could change everything. If you invest in crypto through a Stocks & Shares ISA, you might be able to grow your holdings tax-free up to the £20,000 annual ISA limit. But this doesn’t apply to direct crypto holdings-it only works if you buy crypto via an approved ETN inside an ISA.

HMRC is also considering a ‘de minimis’ rule: no tax on transactions under £1,000. That could help small traders. But as of now, it’s just a proposal. Don’t count on it.

For now, the system is strict, complex, and unforgiving. The UK has gone from being one of the more lenient countries to one of the more demanding. The message from HMRC is clear: if you trade crypto, you’re in the tax system. And they’re ready to collect.

Do I pay tax if I just hold crypto?

No. Simply holding crypto-buying and keeping it-is not a taxable event. Tax is only triggered when you dispose of it: selling, trading, spending, or gifting it. Holding for years without moving it means no tax liability.

What if I lost money on crypto trades?

You can use capital losses to offset future capital gains, but not against your income. If you lost £3,000 this year and make £4,000 next year, you can reduce your taxable gain to £1,000. Losses can be carried forward indefinitely, but you must report them on your tax return to claim them.

Is staking crypto taxable?

Yes. Staking rewards are treated as income and taxed at your marginal rate (20%, 40%, or 45%). You must report the pound value of the reward on the day you received it. Even if you don’t sell the rewards, you still owe tax on them as earned income.

Can I avoid tax by using a non-UK exchange?

No. HMRC taxes UK residents on worldwide income and gains. Whether you use Binance, Coinbase, or a tiny exchange in Estonia, if you’re a UK tax resident, you must report all crypto activity. Exchanges outside the UK are now required to share data with HMRC under international agreements.

What happens if I don’t report my crypto gains?

HMRC has access to data from 47 UK exchanges and is expanding that to global platforms. If you don’t report, they’ll find you. Penalties can range from 30% to 100% of the unpaid tax, plus interest. In serious cases, HMRC can pursue criminal prosecution for tax evasion. It’s not worth the risk.

8 Comments

Ann Liu

Just to clarify the £3,000 CGT allowance-it applies to total gains across all assets, not just crypto. So if you sold a painting for £2,000 and made £1,800 on ETH, you’re already over the limit. Many people don’t realize they’re being taxed on non-crypto disposals too. Keep a running tally. HMRC doesn’t care if you forgot-your records are your responsibility.

Dionne van Diepenbeek

Staking rewards are income period end of story

Bruce Doucette

So let me get this straight-you spent 40 hours tracking transactions so you could pay £90 in tax? 😂 Welcome to the UK tax system, where the government makes you do their accounting for them. At least they don’t charge you for the emotional labor.

rajan gupta

This is why humanity is doomed 🌍💔 We trade digital ghosts for money while the planet burns. The state wants its cut from our dreams. But what is money anyway? Just a shared hallucination. And crypto? A mirror of our collective greed. I lost everything last year... and yet I still hold. Because the system is broken. And I? I am the glitch in the matrix. 💫

Billy Karna

One thing nobody mentions is that the cost basis calculation gets wild when you have partial sells and multiple purchases. HMRC uses the pooled cost method for identical tokens, which means you average all your buys of that coin over time. So if you bought ETH in 2021 at £800, then again in 2023 at £2,500, and again in 2024 at £3,200, and then sold 0.3 ETH in 2025, your cost basis isn’t the price of the last buy-it’s the average of all your purchases. That’s a huge difference. Most people assume FIFO or LIFO, but HMRC doesn’t let you choose. And if you’re using multiple wallets across exchanges? You’re basically doing manual accounting. No wonder 87% of people are overwhelmed. The software isn’t perfect either-it often misses fee allocations or misreads airdrops as income. Always double-check the reports.

Cheri Farnsworth

The requirement to document every single transaction is not merely bureaucratic-it is a foundational element of fiscal integrity. One must maintain precise, contemporaneous records. Failure to do so invites not only financial consequence but moral compromise. The integrity of the system depends on individual responsibility.

Gene Inoue

People complain about paying tax but still hodl 100 ETH like it’s a religion. You want freedom? Then own your tax liability. Stop acting like HMRC is the villain. You’re not a martyr-you’re a taxpayer. And if you can’t handle that, maybe crypto isn’t for you.

Lucy de Gruchy

Let’s be real-this whole system is a scam. HMRC didn’t suddenly get smart. They’re being pressured by the EU and the US to clamp down on crypto because they can’t tax it easily. Meanwhile, banks are laundering billions in crypto through shell companies and nobody bats an eye. But you? You’re the one getting audited for a £500 gain. This isn’t fairness-it’s targeting. And the ‘data sharing’ with global exchanges? That’s not compliance. That’s surveillance. You think your wallet address is private? It’s already in a database somewhere. They’re building the ledger of control. And you’re helping them by using Koinly. Don’t you see it? This is the slippery slope to digital serfdom.