For years, Portugal was the undisputed champion for cryptocurrency investors in Europe. You could buy Bitcoin, hold it, sell it, and pay zero tax on the profits. That golden era ended in 2023. Today, the landscape is sharper, stricter, and demands precision. If you are selling your crypto within a year of buying it, you face a flat 28% short-term crypto tax. But if you can wait just one day longer than that threshold, the tax vanishes completely.

This shift wasn't random. It was part of a broader move to align with European Union standards while trying to keep long-term investors happy. The result is a dual-track system that rewards patience and penalizes speculation. Understanding exactly where you fall on this spectrum-and how to report it-is the difference between keeping your profits and facing a surprise bill from the Autoridade Tributária e Aduaneira (Portuguese Tax Authority).

The 365-Day Rule: Defining Short vs. Long Term

The entire Portuguese crypto tax regime hinges on a single metric: time. Specifically, the holding period. The law draws a hard line at 365 days. This is not a guideline; it is a strict cutoff.

If you dispose of any cryptocurrency-whether by selling it for euros, trading it for another coin, or using it to pay for goods-and you have held that specific asset for less than 365 days, the gain is classified as short-term capital gain. This gain is taxed at a flat rate of 28%. There are no deductions for inflation, no adjustments for market volatility, and no progressive brackets applied to this specific calculation unless you choose otherwise (more on that later).

Conversely, if you hold the asset for more than 365 days before disposal, the capital gain is entirely tax-exempt. This exemption preserves Portugal’s appeal for long-term holders and strategic investors. It creates a powerful incentive to adopt a "buy-and-hold" strategy rather than active day-trading. For many digital nomads and remote workers relocating to Lisbon or Porto, this rule dictates their entire investment portfolio structure.

| Holding Period | Tax Classification | Tax Rate | Reporting Annex |

|---|---|---|---|

| Less than 365 days | Short-Term Capital Gain | Flat 28% | Anexo G |

| More than 365 days | Long-Term Capital Gain | 0% (Exempt) | Anexo G (Declaration only) |

It is crucial to track the exact date of acquisition. For assets acquired through dollar-cost averaging (DCA), each purchase has its own clock. Selling 1 BTC bought in January when you also hold 1 BTC bought in December means you must identify which units you sold. Most exchanges use FIFO (First-In, First-Out) by default, but you may need to provide evidence if you want to claim a different method, though Portuguese authorities generally accept standard accounting practices. Keep records of every transaction hash, timestamp, and euro value at the moment of trade.

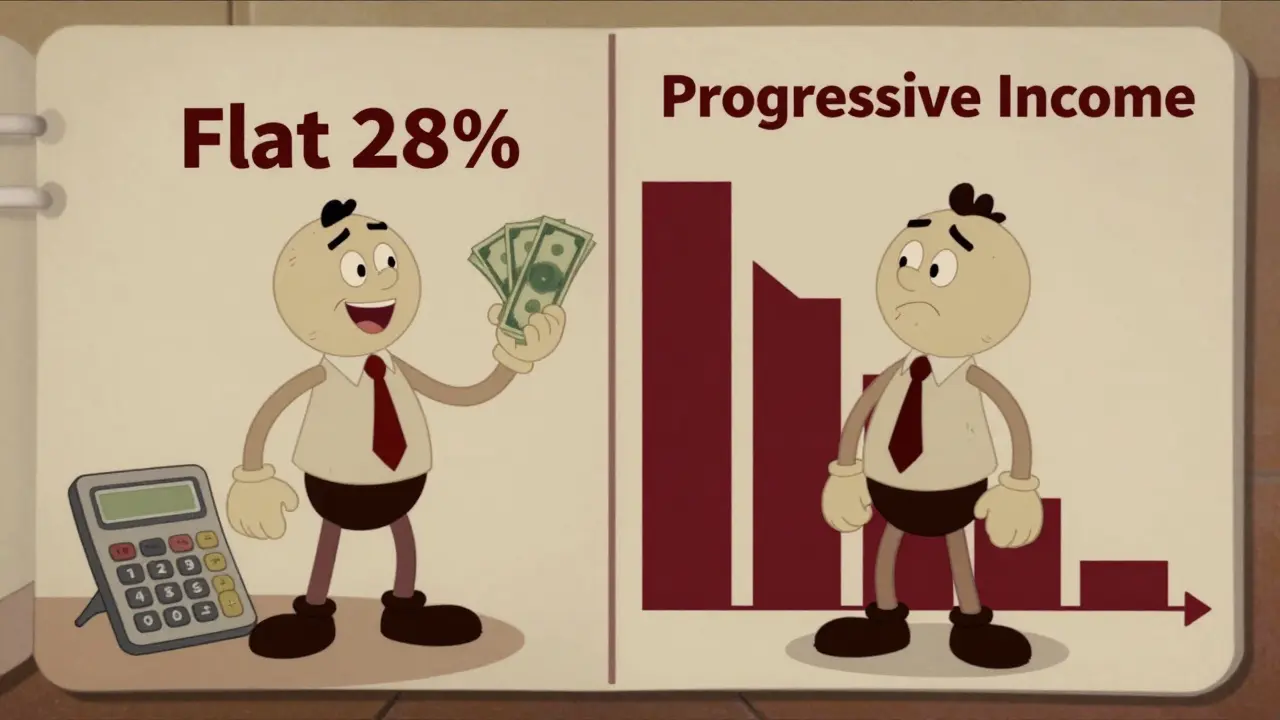

Choosing Your Tax Path: Flat Rate vs. Progressive Income

Here is where it gets interesting. While the default treatment for short-term crypto gains is the 28% flat rate, Portuguese taxpayers have a choice. You can opt to include these crypto gains in your total annual income. This triggers taxation under Portugal’s progressive income tax brackets instead of the flat 28%.

Why would you do this? Because if your overall income is low, the progressive rate might be significantly lower than 28%. In 2024, the lowest bracket starts at 13.25% for income up to €7,703. The next tier is 18%, then 23%, 26%, and so on, climbing all the way to 48% for income exceeding €81,199.

Let’s look at a concrete example. Imagine you earn €15,000 from your job and make €5,000 in short-term crypto profits.

- Option A (Flat Rate): You pay 28% on the €5,000 profit. That is €1,400 in tax.

- Option B (Progressive): Your total income becomes €20,000. The first €15,000 is taxed at your normal rates. The additional €5,000 falls into the 23% bracket (since €15,000 sits between the 18% and 23% thresholds). You would pay roughly 23% on that marginal income, saving yourself money compared to the flat rate.

However, this option works against high earners. If your salary already pushes you into the 45% or 48% bracket, adding crypto gains there would cost you far more than the 28% flat rate. In fact, once your total income exceeds the highest progressive bracket, you are legally obligated to aggregate crypto gains with ordinary income, potentially resulting in higher effective taxes. Always run both calculations before filing your Modelo 3 return.

Passive Income: Staking, Lending, and DeFi Rewards

Selling coins isn't the only way to trigger tax liability. Passive income from cryptocurrency activities is treated differently than capital gains. Rewards from staking, lending platforms, liquidity pools in decentralized finance (DeFi), and even airdrops are considered passive income.

By default, these rewards are subject to the same 28% flat tax rate. They are reported using Anexo E, not Anexo G. This distinction matters because the nature of the income is different. When you receive staking rewards, you are essentially earning interest. The tax authority views this as regular income generation rather than appreciation of an asset's value.

There is a nuance here for professional traders. If you are classified as a professional trader (see below), these rewards might fall under business income rules. But for the average investor, the 28% flat rate applies to the fair market value of the tokens received at the time they hit your wallet. You must declare this value in euros. Do not ignore small amounts; cumulative passive income can add up quickly, especially in high-yield DeFi protocols.

Are You a Professional Trader?

This is the most complex and risky area of Portuguese crypto taxation. If the tax authority determines that your crypto activities constitute a "business," you lose the benefit of the 28% flat rate and the long-term exemption. Instead, your profits are treated as business income, taxed progressively from 14.5% to 53%, plus social security contributions.

How do they decide? There is no single bright line, but authorities look at several factors:

- Frequency: Do you trade daily or weekly?

- Volume: Is the turnover substantial relative to your personal wealth?

- Sophistication: Do you use advanced algorithms, multiple exchanges, or proprietary strategies?

- Primary Source: Is crypto trading your main source of livelihood?

If you answer "yes" to most of these, you likely need to register as a sole proprietor or company. This requires filing Anexo B and paying quarterly advance payments. Many casual traders mistakenly believe they are exempt from this classification because they don't have employees. Having employees is not required to be a business. If you treat crypto like a job, the state will tax you like a business. Consult a local accountant (contabilista) if your trading volume exceeds a few thousand euros per month consistently.

Filing Requirements: Portal das Finanças

All reporting happens through the Portal das Finanças, the online platform of the Portuguese Tax Authority. The main document is the Modelo 3 (annual income tax return), but the annexes are where the details live.

- Anexo G: Used for capital gains. Here you list every disposal. You must specify the acquisition date, disposal date, purchase price, sale price, and the resulting gain or loss. Gains from assets held <12 months go into the taxable section. Gains from assets held >12 months go into the exempt section. Even if exempt, you must declare them to prove compliance.

- Anexo E: Used for passive income. Report staking rewards, lending interest, and other yields here. Apply the 28% withholding tax conceptually, though you pay it directly upon filing.

- Anexo B: Reserved for professional traders. Reports gross revenue minus allowable business expenses.

Deadlines are strict. Typically, the deadline for filing is June 30th of the following year. Late filings incur penalties ranging from €250 to €1,500 per entity, plus interest on unpaid taxes. Use software like CoinLedger or Koinly to generate reports that map directly to these annexes, reducing manual entry errors.

The End of NHR for New Applicants

You cannot discuss Portugal's tax landscape without mentioning the Non-Habitual Residence (NHR) program. Until January 2024, new residents could qualify for NHR, offering significant tax benefits. For existing beneficiaries, foreign-sourced income (which often includes crypto gains if the exchange is outside Portugal) could be taxed at a flat 20% rate or potentially exempt depending on specific treaties and interpretations.

However, the program closed to new applicants in early 2024. If you moved to Portugal after this date, you face the standard rules: 28% for short-term gains, 0% for long-term. This change has cooled the enthusiasm for some digital nomads who previously relied on NHR to optimize their global tax footprint. Existing NHR holders still enjoy their benefits for ten years, creating a two-tier system for residents based on when they arrived.

Comparing Portugal to Neighbors

Despite the 28% tax, Portugal remains competitive in Europe. Compare it to Germany, where short-term gains can be taxed as income up to 45%, or France, which applies a flat 30% tax on all crypto gains regardless of holding period. The UK offers no holding period exemption, taxing gains at up to 20% (capital gains) or 45% (income). Spain taxes savings income at 19-28% but lacks Portugal’s complete long-term exemption.

Portugal’s model strikes a balance. It captures revenue from speculative activity while rewarding long-term commitment. For someone willing to hold Bitcoin for 12 months and one day, Portugal is arguably the best place in the EU to invest. For the day trader, it is merely average.

Is crypto tax-free in Portugal in 2026?

Only if you hold the cryptocurrency for more than 365 days. Any disposal within the first year is subject to a 28% tax on the capital gain. Long-term holdings remain completely tax-exempt.

Do I pay tax on staking rewards?

Yes. Staking rewards are considered passive income and are taxed at a flat 28% rate. You must report these via Anexo E in your annual tax return.

Can I deduct losses from my crypto trades?

Yes. Losses from short-term trades can offset gains from other short-term trades in the same year. Unused losses can often be carried forward to future years, but they cannot offset other types of income like salaries.

What happens if I am a professional trader?

Professional traders are taxed as businesses. Profits are added to your total income and taxed progressively (14.5% to 53%), plus social security contributions. You must file Anexo B and may need to register a company.

Does the NHR program still apply to crypto?

The NHR program closed to new applicants in January 2024. Existing beneficiaries may still enjoy favorable rates (often 20%) on foreign-sourced income for up to 10 years. New residents must follow the standard 28%/0% rule.